How to Handle Debt Management for Small Businesses

Dealing with debt can be a daunting task for small business owners, but it’s crucial to take control of your financial situation in order to ensure the success and longevity of your company. Debt management is a critical aspect of running a business, and it’s important to have a solid plan in place for handling any outstanding debts. In this guide, we will provide you with actionable steps and strategies to effectively manage debt for your small business.

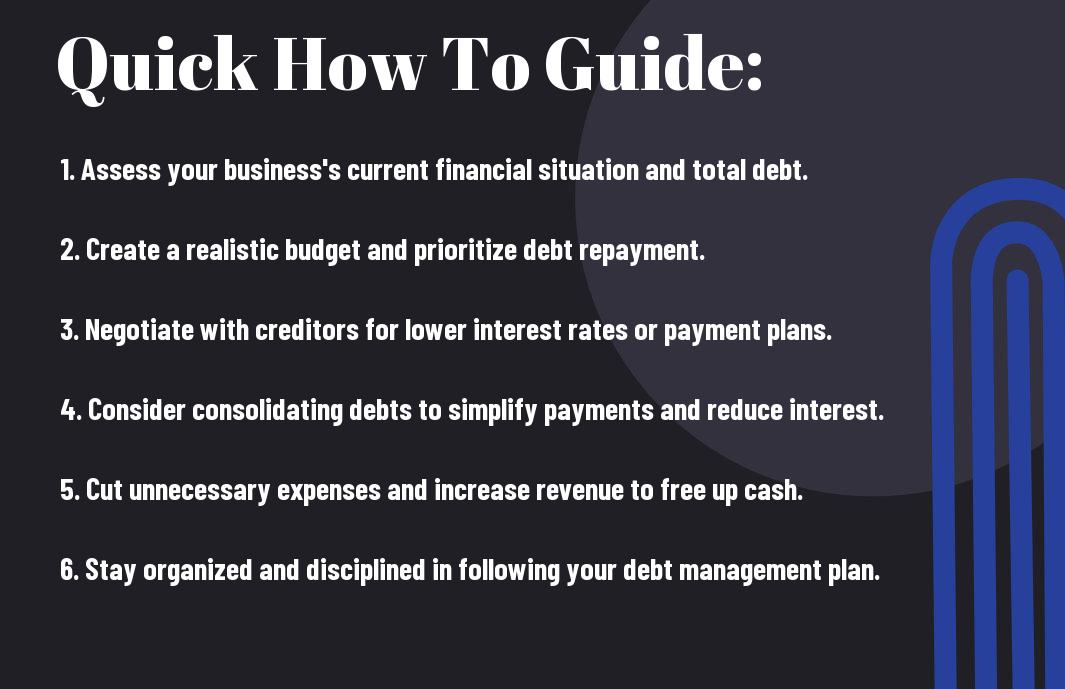

First and foremost, it’s essential to acknowledge your debts and understand the full scope of your financial obligations. This means taking an inventory of all outstanding debts, including loans, credit card balances, and any other liabilities. Once you have a clear understanding of your financial situation, you can begin to develop a debt repayment plan that works for your business. This may involve negotiating payment terms with creditors, prioritizing high-interest debts, and reallocating resources to focus on debt reduction. By taking proactive steps to manage your debts, you can position your business for long-term financial stability and growth.

Key Takeaways:

- Establish a realistic budget: Small businesses must create a comprehensive budget that accounts for all expenses and revenue streams to effectively manage and reduce debt.

- Communicate with creditors: Open and honest communication with creditors can help small businesses negotiate payment terms and potentially reduce interest rates to ease the burden of debt repayment.

- Seek professional guidance when necessary: Small business owners should not hesitate to seek help from financial advisors or debt management professionals to develop a strategy for debt reduction and long-term financial stability.

Evaluating Your Business’s Financial Health

Some of the most important aspects of debt management for small businesses involve evaluating your company’s financial health. This includes understanding your business’s debt-to-income ratio, cash flow, and debt service coverage. By assessing these key financial metrics, you can gain insights into the overall financial stability and solvency of your business.

Calculating Your Debt-to-Income Ratio

When evaluating your business’s financial health, calculating your debt-to-income ratio is a critical step. This ratio represents the amount of your business’s monthly debt payments compared to its monthly income. To calculate your debt-to-income ratio, divide your total monthly debt payments by your gross monthly income. The result will give you a percentage that indicates how much of your income is being used to pay off debt. A high debt-to-income ratio can be a warning sign of financial distress, while a low ratio indicates that your business has more financial flexibility. It’s important to keep your debt-to-income ratio as low as possible to maintain financial stability and improve your ability to handle debt payments.

Analyzing Cash Flow and Debt Service Coverage

Another essential aspect of evaluating your business’s financial health is analyzing your cash flow and debt service coverage. Cash flow represents the amount of money moving in and out of your business, while debt service coverage measures your company’s ability to meet its debt obligations. By examining your cash flow, you can identify any potential cash shortages that may impact your ability to make debt payments. Similarly, analyzing your debt service coverage can help you gauge whether your business generates enough cash to cover its debt obligations. Understanding these metrics can provide you with valuable insights into your business’s financial health and help you make informed decisions about debt management strategies.

How-to: Setting Realistic Debt Management Goals

Your first step in handling debt management for your small business is to set realistic goals. This involves taking a close look at your financial situation, understanding your debts, and creating a plan that is achievable.

Tips for Prioritizing Debts

When it comes to prioritizing debts, it’s important to focus on those with the highest interest rates or those that are long overdue. Start by listing all your debts and their corresponding interest rates. Then, prioritize paying off the ones with the highest rates first to save money in the long run. Another way to prioritize debts is by focusing on those that are past due, as it can negatively impact your business’s credit score and lead to additional fees and penalties if left unpaid.

- Identify debts with the highest interest rates

- Address overdue payments to avoid penalties and credit score damage

Any extra funds should be directed towards paying off these prioritized debts to expedite the process and minimize the overall costs associated with them.

Creating a Timeline for Debt Reduction

Once you’ve prioritized your debts, the next step is to create a timeline for debt reduction. This involves setting specific target dates for paying off each debt based on their priority. Be realistic in your approach, considering your business’s cash flow and budget constraints. It’s important to break down your overall debt reduction goal into smaller, manageable milestones to track your progress and stay motivated.

By creating a timeline, you can hold yourself accountable and ensure that you are making significant strides towards becoming debt-free. This will also help you stay on track and avoid deviating from your debt management goals.

Factors Affecting Debt Management Strategies

For small businesses, it’s important to understand the factors that can affect your debt management strategies. Here are some key considerations to keep in mind:

- Interest rates: fluctuations in interest rates can impact the cost of borrowing and your ability to meet debt obligations

- Business structure: the legal and tax structure of your business can influence how debt is managed and repaid

- Cash flow: the availability of funds to meet debt payments and other business expenses

- Market conditions: changes in the market can impact the ability to generate revenue and repay debts

Assume that these factors can significantly impact your debt management approach and require careful consideration when developing a strategy for your small business.

Interest Rates and Their Role in Debt Management

Interest rates play a crucial role in debt management for small businesses. Fluctuations in interest rates can directly impact the cost of borrowing, affecting your overall debt burden and cash flow. When interest rates rise, the cost of servicing existing debts increases, putting pressure on your finances. Conversely, lower interest rates can make borrowing more affordable, but also come with their own set of challenges. It’s important to carefully monitor and assess the impact of interest rate changes on your debt management strategy to ensure that your business remains financially stable.

The Influence of Business Structure and Tax Obligations

Your business structure and tax obligations can have a significant influence on your debt management approach. The legal and tax structure of your business can affect how debt is managed and repaid. For example, certain business structures may offer more favorable tax treatment for debt financing, which can impact your overall debt strategy. Additionally, tax obligations can impact your cash flow and ability to service debt. It’s essential to consider these factors when developing and implementing your debt management plan to ensure that it aligns with your business’s financial and tax objectives.

How-to: Budgeting for Debt Repayment

Despite the challenges of managing debt for your small business, creating a budget for debt repayment is essential to getting your finances back on track. By following a well-structured plan, you can regain control of your debt and set your business up for financial success. To get started, review the 6 Tips for effective business debt management shared in this article.

Allocating Resources for Monthly Debt Payments

When creating a budget for debt repayment, it’s important to allocate a portion of your monthly resources specifically for debt payments. This ensures that you consistently make progress in paying off your debts. You may need to re-evaluate your current expenses and adjust your cash flow to free up more funds for paying down your debt. By prioritizing debt payments, you can work towards reducing your liabilities and improving your financial position.

Tips for Cutting Expenses to Free Up Funds

If you find that your current budget doesn’t allow for sufficient debt repayment, consider implementing cost-cutting strategies to free up more funds. Look for areas where you can reduce spending, such as renegotiating contracts with suppliers, reducing overhead costs, or consolidating your business loans. Additionally, consider eliminating any non-essential expenses that are not critical to the operation of your business. By optimizing your budget and cutting unnecessary costs, you can create more room to allocate towards debt repayment. Any extra funds you can put towards debt will help you make progress more quickly.

Negotiation Strategies with Creditors

Not all businesses are able to meet their debt obligations on time, and sometimes, negotiating with creditors becomes necessary. This chapter will guide you through effective negotiation strategies and tips for handling debt with your creditors.

How to Approach Creditors for Better Terms

When approaching your creditors for better terms, it’s important to be prepared. Start by analyzing your current financial situation and creating a realistic repayment plan that you can present to your creditors. This will show them that you are serious about addressing the debt and are committed to finding a solution. When you approach your creditors, be transparent and honest about your financial difficulties. Explain your situation and the reasons for the challenges you are facing. By demonstrating your willingness to work with them, you can build credibility and trust. Lastly, be ready to negotiate and be open to compromise. Consider proposing a lower interest rate, extended payment terms, or reduced principal amount to make the debt more manageable for your business.

The Pros and Cons of Debt Settlement

Debt settlement can be an effective way to reduce your debt burden, but it’s important to understand the potential advantages and disadvantages before pursuing this option.

| Pros | Cons |

| Reduction of overall debt amount | Potential negative impact on credit score |

| Opportunity to resolve debt quickly | Possible tax implications |

| Avoidance of bankruptcy | Potential for legal actions by creditors |

It’s important to weigh the pros and cons carefully to determine if debt settlement is the right option for your business. While it can provide relief from overwhelming debt, it can also have long-term consequences. You should consider consulting with a financial advisor or legal expert to understand the implications and explore alternative solutions.

Exploring Debt Consolidation and Restructuring

Now that you understand the basics of debt management for small businesses, it’s time to explore the options available to you. One common approach to handling business debt is through debt consolidation and restructuring. These methods can help you manage your debt more effectively and create a path towards financial stability for your business.

Is Debt Consolidation Right for Your Business?

If you are struggling to keep up with multiple debt payments and high-interest rates, debt consolidation may be a viable option for your small business. Consolidating your debts involves taking out a new loan to pay off your existing debts, combining them into a single, more manageable payment. By doing so, you can potentially lower your overall interest rate and simplify your repayment process. However, it’s important to carefully assess whether debt consolidation is the right choice for your business, as it may involve using collateral or result in extending the repayment period, increasing the total interest paid over time.

The Process of Restructuring Business Debt

When your business is struggling with debt, restructuring can be an effective way to negotiate new terms with your creditors. This may involve reducing the amount of debt owed, lower interest rates, or extending the repayment period. However, the process is complex and may require professional assistance to navigate successfully. It’s important to understand that debt restructuring can have significant implications for your business, potentially affecting your credit rating and relationship with creditors. Before proceeding with debt restructuring, it’s crucial to carefully weigh the potential benefits against the risks involved.

Preventative Measures and Avoiding Future Debt

Unlike reactive measures that focus on resolving current debt issues, preventative measures involve taking steps to avoid accumulating future debt. By implementing the following strategies, you can safeguard your small business from falling into the pitfalls of excessive debt.

Tips for Better Credit Management

When it comes to credit management, a crucial step is to maintain a good credit score. This can be achieved by making timely payments on your business loans and credit lines. Additionally, you should regularly review your credit report to identify any errors or discrepancies that could affect your score. Another key aspect of credit management is to keep your credit utilization low. This means that you should aim to use only a small portion of your available credit. Monitor your credit utilization regularly to ensure that it remains within a healthy range. Perceiving your credit as a valuable asset and managing it responsibly can help you avoid unnecessary debt in the future.

- Make timely payments on your loans and credit lines

- Regularly review your credit report for errors

- Keep your credit utilization low

- Monitor your credit utilization regularly

How to Build an Emergency Fund

Having an emergency fund can provide you with a safety net to cover unexpected expenses and mitigate the need for taking on additional debt. To build an emergency fund, you should set aside a portion of your business profits on a regular basis. Creating a separate savings account specifically for your emergency fund can help you avoid dipping into these funds for non-urgent expenses. By consistently contributing to your emergency fund, you can prepare your business for any unexpected financial challenges that may arise.

Conclusion

Hence, it is crucial for you to have a clear and realistic debt management plan in place for your small business. By properly managing your debt, you can avoid potential financial strain and maintain a healthy cash flow. It is important to regularly review your debts, negotiate with lenders, and seek professional advice if necessary to ensure that you are effectively managing your business’s debt.

Remember that proper debt management is essential for the long-term success and growth of your small business. By taking control of your debt and managing it effectively, you can minimize financial risk and position your business for future success. Stay proactive and diligent in your debt management efforts, and you will ultimately benefit from a more stable and prosperous business.

Debt Management for Small Businesses FAQ

Q: What is debt management for small businesses?

A: Debt management for small businesses refers to the process of effectively managing and paying off business debts in order to maintain financial stability and avoid bankruptcy or insolvency. It involves creating a plan to address existing debts, as well as implementing strategies to prevent the accumulation of future debts.

Q: Why is debt management important for small businesses?

A: Debt management is crucial for small businesses as excessive debts can hinder growth, lead to financial instability, and even result in the closure of the business. By actively managing debts, small businesses can improve cash flow, maintain a positive credit score, and ensure the long-term success of the business.

Q: What are some strategies for effective debt management for small businesses?

A: Some strategies for effective debt management for small businesses include creating a budget and cash flow analysis, negotiating with creditors for better repayment terms, prioritizing high-interest debts, and exploring debt consolidation or refinancing options. Additionally, implementing strict credit policies and reducing unnecessary expenses can help prevent the accumulation of additional debts.

Q: How can small businesses prioritize which debts to pay off first?

A: Small businesses should prioritize paying off high-interest debts first in order to minimize the overall cost of debt. Additionally, debts that are secured by collateral or those owed to essential suppliers or vendors should be prioritized to avoid potential legal action or disruption of business operations. It’s important to consistently make at least the minimum payments on all debts to avoid negative consequences such as penalties and damaged credit.

Q: When should small businesses seek professional assistance for debt management?

A: Small businesses should consider seeking professional assistance for debt management if they are struggling to keep up with debt payments, are facing legal action from creditors, or are experiencing cash flow issues due to high levels of debt. Professional debt management services can provide expert guidance, negotiate with creditors on behalf of the business, and help develop a comprehensive debt repayment plan tailored to the specific needs of the business.