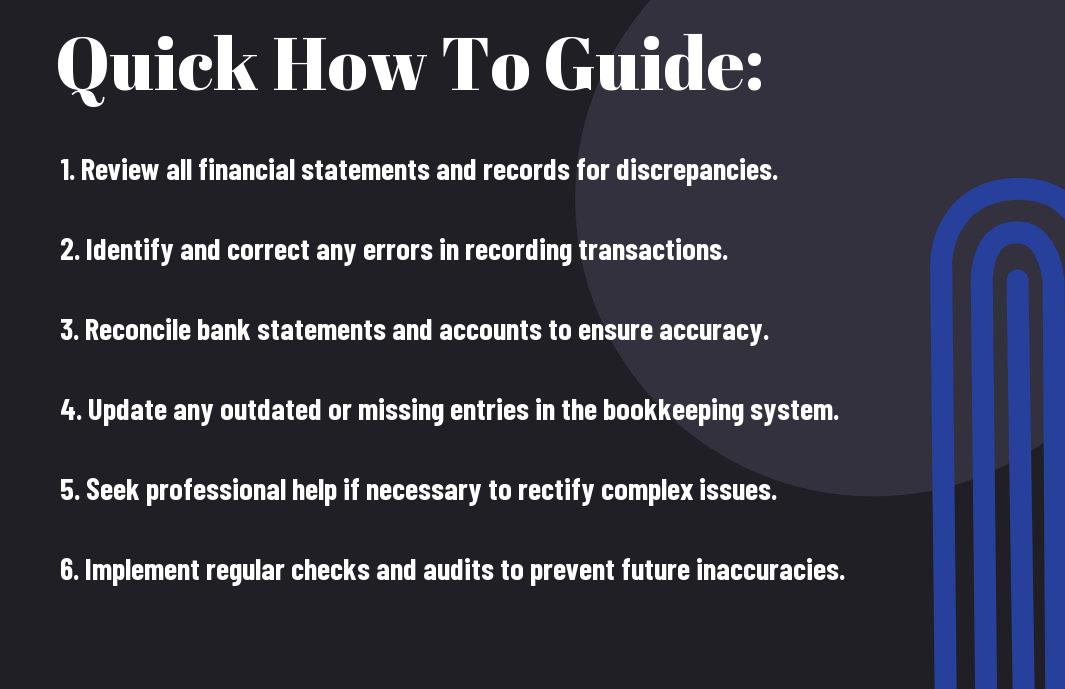

How to Fix Inaccurate Bookkeeping in Your Small Business

Are you struggling with inaccurate bookkeeping in your small business? It’s essential to address this issue as soon as possible to ensure the financial health and success of your company. Inaccurate bookkeeping can lead to serious consequences that can negatively impact your business, including missed tax deadlines, cash flow problems, and even legal issues. To understand the severity of the situation, check out this article on 10 Consequences of Bad Bookkeeping in Your Business.

Luckily, there are steps you can take to fix inaccurate bookkeeping and regain control of your financial records. In this blog post, we will provide you with practical tips and strategies to rectify any mistakes in your bookkeeping and prevent future inaccuracies. By following these steps, you can ensure that your small business is on the right track towards financial stability and success.

Key Takeaways:

- Regular Reconciliation: Regular reconciliation of accounts is crucial to identify and rectify any discrepancies in bookkeeping.

- Utilize Accounting Software: Invest in accounting software to streamline bookkeeping processes and reduce the chances of inaccuracies.

- Seek Professional Help: If your bookkeeping errors are recurring or complex, consider seeking professional help from a bookkeeper or accountant to address and correct the inaccuracies.

Identifying Bookkeeping Inaccuracies

Any small business owner knows the importance of accurate bookkeeping. However, mistakes happen, and they can have serious consequences for your business. It’s essential to be able to identify these inaccuracies so you can rectify them quickly and avoid any potential negative impact on your business.

Common Bookkeeping Mistakes

One of the most common bookkeeping mistakes is failing to reconcile your bank statements regularly. This can lead to discrepancies between your books and your actual bank balance, causing confusion and potential errors in your financial records. Another common mistake is not categorizing transactions correctly, which can make it difficult to track expenses and revenues accurately.

Tools for Error Detection

One of the best tools for error detection in bookkeeping is a reliable accounting software. These programs can help you detect discrepancies and inaccuracies in your financial records by generating reports and alerts for potential errors. Additionally, using bank feeds can help you reconcile your accounts more easily, as they provide real-time data that can help you identify any discrepancies.

By using these tools and being aware of the most common bookkeeping mistakes, you can improve the accuracy of your financial records and make better-informed business decisions. It’s crucial to stay diligent in identifying and rectifying any inaccuracies to ensure the financial health of your small business.

Setting the Stage for Correction

For many small business owners, inaccurate bookkeeping can be a nightmare. It can lead to financial losses, tax penalties, and even legal troubles. However, all hope is not lost. By taking the right steps, you can fix inaccurate bookkeeping and get your business back on track. The first step in this process is to set the stage for correction by establishing a timeline for revision and organizing your financial documents.

Establishing a Timeline for Revision

When it comes to fixing inaccurate bookkeeping, it’s crucial to establish a timeline for revision. You need to go through your financial records and identify the specific periods where inaccuracies occurred. This could involve looking at bank statements, invoices, receipts, and any other financial documents to pinpoint the exact dates or periods where errors were made. By doing so, you’ll be able to focus your efforts on rectifying the mistakes and preventing them from happening again in the future.

Depending on the severity of the inaccuracies, you may need to work on revising your bookkeeping on a monthly, quarterly, or yearly basis. It’s important to be thorough in this process and not rush through it, as overlooking even the smallest detail can lead to further complications down the line.

Organizing Financial Documents

Another essential step in setting the stage for correction is to organize your financial documents. This means gathering all relevant paperwork, such as invoices, receipts, bank statements, and tax records, and arranging them in a systematic manner. You may want to create separate folders or digital files for each financial year or quarter to make it easier to track and review your records.

Organizing your financial documents will not only streamline the revision process but also help you gain a clearer understanding of your business’s financial health. It will enable you to identify patterns and discrepancies more effectively, ultimately allowing you to make more informed decisions moving forward.

By establishing a timeline for revision and organizing your financial documents, you can lay the groundwork for fixing inaccurate bookkeeping in your small business. These steps will help you gain clarity on the extent of the inaccuracies and provide a solid foundation for making necessary corrections. Remember that attention to detail and thoroughness are key in this process, so take the time to ensure you’ve covered all bases before proceeding.

Engaging in Error Correction Techniques

Unlike preventing errors in bookkeeping, correcting inaccuracies requires a different set of techniques. It’s essential to approach error correction in a methodical and systematic manner to ensure that all discrepancies are resolved accurately and efficiently. Engaging in error correction techniques involves two primary steps: reconciling accounts and adjusting ledger entries.

How-to Guide for Reconciling Accounts

Reconciling accounts is a crucial step in fixing inaccurate bookkeeping. Start by comparing your bank statements with your financial records to identify any discrepancies. Match each transaction in your accounting records with the corresponding entry in your bank statement. If you discover any variances, investigate the reasons behind them. This could include bank fees, unauthorized transactions, or errors in your records. By meticulously comparing and reconciling your accounts, you can identify and rectify any inaccuracies.

Tips for Adjusting Ledger Entries

When addressing inaccurate bookkeeping, you may need to adjust ledger entries to reflect the correct financial data. One tip for adjusting ledger entries is to document all modifications thoroughly. This includes providing a clear explanation for each adjustment and obtaining appropriate authorization. Additionally, it’s crucial to maintain an audit trail to track the changes made to your ledger entries. This ensures transparency and accountability in your bookkeeping processes. Assume that all adjustments are subject to scrutiny, and therefore, accuracy and precision are paramount.

- Document all modifications: Provide a clear explanation for each adjustment and obtain appropriate authorization.

- Maintain an audit trail: Track the changes made to your ledger entries to ensure transparency and accountability.

- Assume that all adjustments are subject to scrutiny, accuracy and precision are paramount.

Implementing Strong Bookkeeping Practices

To fix inaccurate bookkeeping in your small business, you need to implement strong bookkeeping practices. This involves setting up effective systems, training your team, and staying on top of your financial records. Here are some key factors to consider when implementing strong bookkeeping practices.

Factors Contributing to Effective Bookkeeping

One of the key factors contributing to effective bookkeeping is consistency. You need to ensure that your financial records are updated regularly and accurately. This means recording all transactions, reconciling accounts, and reviewing financial reports on a consistent basis. Another important factor is attention to detail. Small errors in bookkeeping can lead to major inaccuracies down the line, so it’s crucial that you and your team pay close attention to the details of every transaction. Additionally, organization plays a vital role in effective bookkeeping. By keeping your financial documents and records organized, you can easily access important information and prevent errors or omissions.

- Consistency: Recording all transactions, reconciling accounts, and reviewing financial reports regularly.

- Attention to detail: Paying close attention to the details of every transaction to avoid errors.

- Organization: Keeping financial documents and records organized to prevent errors or omissions.

After implementing these factors, you can ensure accuracy and reliability in your small business’s bookkeeping practices.

Training and Resources for Your In-house Team

Investing in the training and resources for your in-house team is essential for maintaining accurate bookkeeping practices in your small business. By providing your team with the necessary training, you can enhance their understanding of bookkeeping principles and accounting software. This will enable them to perform their bookkeeping duties with greater efficiency and accuracy. Additionally, providing access to resources such as online tutorials, webinars, and reference materials can help your team stay updated on the latest bookkeeping practices and regulations.

Moreover, it’s important to empower your team by offering ongoing support and encouragement. This will motivate them to take ownership of their bookkeeping responsibilities and strive for excellence in maintaining accurate financial records for your small business.

Utilizing Technology to Enhance Accuracy

Your small business can greatly benefit from utilizing technology to enhance the accuracy of your bookkeeping. With the right tools and software solutions, you can streamline your processes and reduce the risk of inaccuracies in your financial records.

Software Solutions for Small Business Bookkeeping

When it comes to bookkeeping, there are numerous software solutions available that can help you keep your records accurate and up to date. QuickBooks and Xero are popular options that provide features such as automated invoicing, expense tracking, and financial reporting. These platforms are user-friendly and can be customized to suit the specific needs of your business. By investing in a reliable software solution, you can save time and minimize human error in your bookkeeping processes.

Automation Tips for Recurring Transactions

Implementing automation for recurring transactions is another effective way to improve the accuracy of your bookkeeping. Set up automatic bank feeds to import your financial data directly into your accounting software, eliminating the need for manual data entry. Additionally, consider using recurring invoice templates to automate the billing process for regular clients and customers. This not only saves time but also reduces the risk of forgetting to bill for services rendered. Furthermore, you can schedule automated payments for recurring expenses, ensuring that your bills are paid on time without the risk of oversight. This proactive approach to automation can significantly improve the accuracy of your financial records.

- Automated bank feeds for importing financial data

- Recurring invoice templates for automated billing

- Automated payments for recurring expenses

This proactive approach to automation can significantly improve the accuracy of your financial records.

Monitoring and Reviewing Financial Records

Not keeping track of your financial records on a regular basis can lead to inaccuracies and potential financial disasters in your small business. It’s critical to monitor and review your financial records to ensure the health and stability of your business.

Scheduling Regular Bookkeeping Audits

Scheduling regular bookkeeping audits is essential for maintaining accurate financial records in your small business. You should set aside time every month to review your accounts, transactions, and financial statements thoroughly. During this process, you can identify any discrepancies or errors that may have occurred and take corrective action promptly. It’s also a good opportunity to update your financial records with any new information or changes that have occurred during the month.

Tips for Effective Financial Review and Analysis

When reviewing and analyzing your financial records, there are several key tips to keep in mind. Firstly, you should ensure that all transactions are accurately recorded and categorized. This includes keeping detailed records of all income and expenses, as well as reconciling bank and credit card statements. Secondly, you should regularly review your financial statements, such as your balance sheet and income statement, to gain a comprehensive understanding of your business’s financial health.

- Regularly reconcile your accounts to identify and correct any discrepancies.

- Keep a close eye on your cash flow to ensure you have enough funds to cover expenses and investments.

Assume that inaccurate bookkeeping can lead to serious financial repercussions for your business. Therefore, it’s crucial to stay on top of your financial records and regularly review and analyze them to ensure accuracy and stability.

Learning from Mistakes and Maintaining Accurate Books

Now that you have identified and resolved the inaccuracies in your bookkeeping, it’s important to learn from your mistakes and take steps to maintain accurate records in the future. By doing so, you can avoid similar issues from arising again in the future. Learning from your mistakes will help you improve your bookkeeping practices and ensure the financial health of your small business.

How to Use Errors as Learning Opportunities

When you encounter errors in your bookkeeping, it’s essential to view them as learning opportunities. Take the time to analyze the mistakes and understand how they occurred. Did they result from a lack of attention to detail, a misunderstanding of accounting principles, or simply human error? By identifying the root cause of the inaccuracies, you can implement preventive measures to avoid similar issues in the future. Additionally, consider seeking assistance from a professional accountant or bookkeeper who can provide guidance and support in maintaining accurate books.

Strategies for Long-Term Bookkeeping Accuracy

To maintain accurate bookkeeping in your small business, consider implementing strategies that will promote long-term accuracy. This may include utilizing accounting software to automate processes, conducting regular reconciliations of your accounts, and establishing a clear system for organizing and categorizing financial transactions. It’s also important to stay informed about any changes in tax laws or accounting regulations that may impact your record-keeping practices. By staying proactive and diligent in your approach to bookkeeping, you can ensure the financial stability of your business and make informed decisions based on accurate financial data.

Conclusion

Presently, you have learned the importance of accurate bookkeeping in your small business and the potential consequences of inaccurate financial records. By following the steps outlined in this guide, you can effectively identify and rectify any bookkeeping errors that may be impacting your business. It is crucial to regularly reconcile your accounts, keep detailed financial records, and seek professional help if necessary in order to maintain accurate bookkeeping and ensure the financial health of your small business.

Remember that accurate bookkeeping is not only essential for compliance and tax purposes, but it also provides valuable insights into the financial performance of your business. By addressing any inaccuracies in your bookkeeping, you can make informed financial decisions and ultimately improve the overall success and stability of your small business. By taking proactive steps to fix inaccurate bookkeeping, you can set your business up for long-term success and growth.

FAQ

Q: What are the signs of inaccurate bookkeeping in a small business?

A: Signs of inaccurate bookkeeping may include missing or duplicate transactions, inconsistent account balances, and unexplained discrepancies in financial reports.

Q: How can inaccurate bookkeeping negatively impact a small business?

A: Inaccurate bookkeeping can lead to incorrect financial statements, tax penalties, and poor decision-making due to unreliable data.

Q: What steps can I take to fix inaccurate bookkeeping in my small business?

A: You can start by conducting a thorough review of your financial records, reconciling accounts, and implementing a standardized bookkeeping process. It’s also advisable to seek the assistance of a professional accountant or bookkeeper.

Q: How often should I review my small business’ bookkeeping to ensure accuracy?

A: It’s recommended to review your bookkeeping on a monthly basis to identify and rectify any inaccuracies promptly. Additionally, an annual audit by a certified public accountant can provide a comprehensive check of your financial records.

Q: What tools or software can help improve the accuracy of bookkeeping in my small business?

A: Utilizing accounting software such as QuickBooks, Xero, or FreshBooks can streamline your bookkeeping processes and reduce the likelihood of errors. These tools offer features such as bank reconciliation, automated invoicing, and financial reporting to aid in accurate record-keeping.