How to Create and Implement Credit Management Strategies for Small Business Success

Are you looking to optimize the financial health of your small business? One crucial aspect to consider is your credit management strategies. Effective credit management can make or break a small business, impacting everything from cash flow to vendor relationships. In this guide, you will learn key steps to developing and executing credit management strategies that will set your small business up for success.

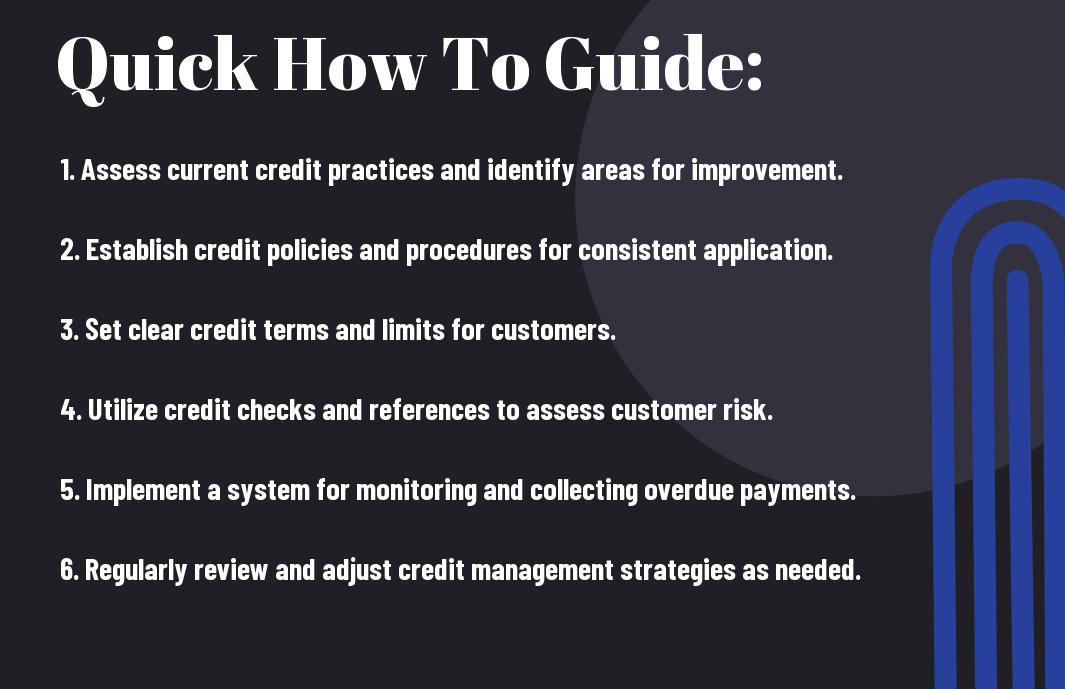

First, it is important to assess the current state of your business’s credit management. This includes conducting a thorough review of your credit policies and procedures, as well as assessing your current outstanding balances and delinquent accounts. From there, you can begin to identify opportunities for improvement and develop a plan for implementing new credit management strategies. By taking proactive measures to manage and monitor your small business’s credit, you can ensure a healthy financial future for your company.

Key Takeaways:

- Understand your business’s credit needs: Assess your business’s credit needs and create a clear strategy to meet those needs. This may involve establishing credit lines, managing customer credit, and understanding your own credit history.

- Implement effective credit management techniques: Use a combination of tools such as credit checks, invoicing practices, and clear payment terms to manage your business’s credit effectively. This can help reduce the risk of late payments and bad debts.

- Regularly review and adjust your credit management strategy: Regularly monitor your business’s credit management performance and adjust your strategies as needed. This can help you stay proactive in managing credit risks and improving your overall financial health.

Fundamentals of Credit Management

If you own a small business, it’s crucial to have a solid understanding of the fundamentals of credit management. This involves the assessment, monitoring, and control of the credit extended to your customers. Effective credit management is essential for maintaining positive cash flow and minimizing the risk of bad debt.

Key Factors Influencing Credit Risk

If you want to successfully manage credit within your small business, it’s important to consider the key factors that influence credit risk. Creditworthiness, industry trends, and economic conditions all play a significant role in determining the level of risk associated with extending credit to your customers. Additionally, the financial stability of your customers, as well as their payment history, can also impact their credit risk. It’s important to thoroughly assess these factors before extending credit to ensure you minimize the risk of non-payment.

- Creditworthiness: Assessing the financial stability and credit history of your customers is crucial in determining their credit risk.

- Industry Trends: Understanding the overall health and trends within your customer’s industry can provide insight into their ability to make timely payments.

- Economic Conditions: External economic factors can impact your customer’s ability to pay. Stay informed about economic conditions that can affect your customer base.

Though assessing credit risk can be complex, understanding these key factors will help you make informed decisions when extending credit to your customers.

Establishing a Credit Policy Framework

When it comes to credit management for your small business, establishing a credit policy framework is essential. This framework encompasses the guidelines and procedures for evaluating potential customers, determining credit terms, and managing collections. Your credit policy should outline the criteria for extending credit, credit limits, and the process for recovering overdue payments. It’s important to take into account the specifics of your business, including industry standards, cash flow needs, and risk tolerance when establishing your credit policy.

Having a clear credit policy framework in place not only ensures consistency in credit decisions but also helps minimize the risk of non-payment and maintain positive customer relationships.

How to Assess Creditworthiness

Not all customers are worthy of extending credit to. Assessing the creditworthiness of potential and existing customers is a crucial step in managing credit effectively for your small business. By implementing a thorough assessment process, you can minimize the risk of late payments, defaults, and bad debt, ultimately contributing to the financial health and success of your business.

Tips for Conducting Customer Credit Checks

When it comes to assessing creditworthiness, conducting customer credit checks is essential. This process involves evaluating the financial stability and payment history of your customers to determine their ability and likelihood to pay you back on time. Here are some tips for conducting effective customer credit checks:

- Obtain permission: Before obtaining any financial information, ensure that you have obtained the necessary consent from your customers. This can be done through a credit application or in your terms and conditions.

- Utilize credit reporting agencies: Verify the creditworthiness of potential customers by obtaining their credit reports from reputable credit reporting agencies. These reports can provide valuable information about their payment history, outstanding debts, and credit utilization.

- Stay updated: Regularly monitor the credit status of your existing customers. This will enable you to identify any changes in their financial circumstances that may impact their ability to fulfill their payment obligations to your business.

Perceiving any warning signs early on can help you make informed decisions about whether to extend credit to a customer or adjust their credit limits.

Analyzing Financial Statements and Credit Reports

Another essential aspect of assessing creditworthiness is analyzing the financial statements and credit reports of your customers. By closely examining this information, you can gain valuable insights into their financial stability and behavior. When analyzing financial statements and credit reports, pay attention to key financial ratios, outstanding debts, payment patterns, and any negative remarks or legal actions. This thorough review will provide you with a comprehensive understanding of your customers’ creditworthiness, enabling you to make more informed decisions when it comes to extending credit and setting payment terms.

Strategies for Effective Credit Management

To ensure the success of your small business, it is crucial to have effective credit management strategies in place. These strategies will help you maintain a healthy cash flow, reduce the risk of bad debt, and build strong relationships with your customers.

Setting Credit Limits: Factors and Methods

When it comes to setting credit limits for your customers, there are several factors to consider. First, you need to assess the financial stability of the customer, including their credit history, payment behavior, and overall financial health. You should also take into account the nature of the business, the industry they operate in, and any seasonal fluctuations that may affect their cash flow. Additionally, consider the amount of credit that your small business can afford to extend without putting your own financial stability at risk. The methods for setting credit limits can vary, but commonly include using a percentage of the customer’s sales volumes or based on their credit score. Implementing a credit limit policy that includes regular reviews and adjustments based on customer behavior and business changes can help ensure that you are not overextending credit to risky customers.

The key to successful credit limit setting lies in finding the right balance between offering enough credit to encourage sales and minimizing the risk of non-payment. Regular monitoring and evaluation of customer credit performance can help you make necessary adjustments and identify any potential issues early on.

How to Develop a Risk-Based Pricing Model

Implementing a risk-based pricing model can be an effective strategy for managing credit risk. You can develop a risk-based pricing model by taking into consideration the creditworthiness of your customers and adjusting your pricing or payment terms accordingly. This can help you mitigate the risk of non-payment by charging higher prices or requiring shorter payment terms for higher-risk customers. On the other hand, you can offer lower prices or more flexible payment terms to lower-risk customers, attracting more business while minimizing the risk of bad debts. By developing a risk-based pricing model, you can align your pricing and credit policies with the level of risk associated with each customer, ensuring that you are adequately compensated for the risk you take on.

Implementing a Credit Management Process

Despite the size of your business, it is important to have a well-defined credit management process in place to ensure the financial health of your company. Developing and implementing a credit management process will help you minimize the risk of non-payment and improve cash flow, ultimately contributing to the success of your small business. To learn more about how to develop a credit policy, you can refer to How to Develop a Credit Policy.

Designing and Documenting the Credit Approval Process

When designing a credit approval process, it is crucial to clearly outline the steps that need to be taken for credit evaluation and approval. This includes establishing criteria for assessing the creditworthiness of potential customers, as well as the documentation required for the credit application process. It is essential to document the process to ensure consistency and compliance with your credit policy. By doing so, you can streamline the approval process and minimize the risk of granting credit to customers who may not be able to fulfill their financial obligations to your business.

Creating a Credit Management Team Structure

Having a structured credit management team in place is vital for the success of your credit management process. By creating roles and responsibilities within the team, you can ensure that each aspect of the credit management process is adequately covered. This includes assigning tasks such as credit evaluation, collections, and customer communications. By establishing a clear team structure, you can effectively manage credit risk and maintain a healthy cash flow for your small business. Additionally, having a dedicated team in place allows for prompt and efficient handling of credit-related matters, ultimately benefiting your company’s bottom line.

Managing Credit Accounts

Keep a close eye on your credit accounts to ensure that your business has a healthy cash flow. Late payments and defaults can significantly impact your business, so it’s important to stay on top of your credit management strategies.

Tips for Monitoring Customer Credit Terms

When managing your credit accounts, it’s important to monitor your customer credit terms closely. Be sure to review customer credit applications thoroughly and check their credit references. Keep an eye on the aging report for any overdue payments and follow up promptly. Utilize a credit scoring system to assess your customers’ creditworthiness and set appropriate credit limits. Additionally, consider implementing a credit monitoring service to keep track of any changes in your customers’ credit profiles.

- Regularly review customer credit applications and references.

- Monitor the aging report for overdue payments.

- Utilize a credit scoring system for creditworthiness assessment.

- Consider a credit monitoring service for changes in customer credit profiles.

Knowing your customers’ credit history and payment patterns can help you make informed decisions about extending credit terms and minimize the risk of late payments or defaults.

Handling Late Payments and Defaults

One of the challenges of managing credit accounts is dealing with late payments and defaults. It’s essential to have clear policies in place for handling these situations. Communicate your payment terms clearly to your customers, and send out reminders for overdue payments. Establish a process for handling late payments, such as charging late fees or interest. In the case of defaults, be prepared to take action to recover the outstanding debt, whether through internal collections or third-party agencies.

It’s important to address late payments and defaults promptly to minimize their impact on your business. Consider implementing a proactive approach, such as offering early payment discounts or setting up payment plans for customers experiencing financial difficulties. By effectively managing late payments and defaults, you can protect your business’ financial health and maintain positive relationships with your customers.

Using Technology in Credit Management

Your small business can greatly benefit from using technology to streamline your credit management processes. By leveraging credit management software and integrating credit tools with your existing business systems, you can effectively monitor and improve your credit management strategies, leading to better financial health and success for your business.

How to Leverage Credit Management Software

When it comes to managing credit for your small business, having the right software can make all the difference. With credit management software, you can automate many of your credit-related tasks, such as issuing invoices, tracking payments, and sending reminders for overdue payments. This not only saves you time, but also ensures that you stay on top of your credit management responsibilities.

Furthermore, credit management software often comes with features that allow you to assess the creditworthiness of your customers, set credit limits, and create customized payment plans. This can help you minimize the risk of extending credit to customers who may not be able to pay on time, ultimately reducing the likelihood of bad debt for your business.

Integrating Credit Tools with Business Systems

Integrating credit tools with your existing business systems can improve efficiency and accuracy in your credit management processes. By connecting credit management software with your accounting, customer relationship management (CRM), and sales systems, you can ensure that credit-related information is seamlessly shared across your organization.

This integration can streamline your workflow and provide you with a comprehensive view of your customers’ credit history, payment behavior, and outstanding balances. With this holistic view, you can make informed decisions about extending credit, setting payment terms, and managing collection efforts, ultimately improving your cash flow and minimizing credit risk for your business.

Maintaining Legal and Ethical Credit Practices

Unlike large corporations, small businesses often lack the legal and financial resources to navigate complex credit laws and regulations. However, it is crucial for the success of your business to maintain legal and ethical credit practices. By doing so, you not only ensure compliance with the law but also build trust with your customers and partners.

Understanding Regulations and Compliance Issues

When it comes to credit management, it’s essential to understand the regulations and compliance issues that apply to your small business. This includes familiarizing yourself with the Fair Credit Reporting Act (FCRA), Equal Credit Opportunity Act (ECOA), and other relevant laws. By doing so, you can ensure that your credit practices align with legal requirements, avoiding the risk of costly penalties and lawsuits. Additionally, staying updated on changes in regulations and compliance issues will enable you to adapt your credit management strategies accordingly, keeping your business in good standing.

How to Craft Fair and Transparent Credit Practices

Crafting fair and transparent credit practices is not only a legal necessity but also a way to establish trust and credibility with your customers. You should clearly communicate your credit terms and policies, including interest rates, fees, and repayment terms. This transparency not only protects your business from potential disputes or misunderstandings but also demonstrates your commitment to ethical business practices. By treating your customers fairly and transparently, you can build a positive reputation and foster long-term customer relationships, ultimately driving the success of your small business.

Conclusion

Conclusively, implementing effective credit management strategies is crucial for the success of your small business. By creating a clear credit policy, regularly monitoring your customers’ creditworthiness, and communicating effectively with them about payment terms, you can ensure that your business has a steady cash flow and minimize the risk of bad debt. Additionally, offering incentives for early payment and utilizing credit management software can streamline the process and make it easier for you to stay on top of your credit management efforts.

Remember, it’s important to regularly review and revise your credit management strategies to adapt to changes in your business and the external market. By taking a proactive approach to credit management, you can set your small business up for long-term success and reduce the likelihood of financial instability due to late or non-payment from customers.

FAQ

Q: Why is credit management important for small businesses?

A: Credit management is crucial for small businesses as it helps in maintaining a healthy cash flow, reducing bad debt, and ensuring timely payments from customers. By implementing effective credit management strategies, small businesses can minimize financial risks and improve their overall financial health.

Q: What are the key components of a credit management strategy for small businesses?

A: The key components of a credit management strategy for small businesses include credit assessment of customers, setting credit limits, establishing clear payment terms, monitoring customer payments, and implementing a collections process for overdue accounts. These components work together to help small businesses manage credit effectively.

Q: How can small businesses assess the creditworthiness of their customers?

A: Small businesses can assess the creditworthiness of their customers by conducting background checks, obtaining trade references, analyzing previous payment history, and using credit reporting agencies. These methods help in determining the risk associated with extending credit to specific customers.

Q: What are some best practices for implementing credit management strategies in small businesses?

A: Some best practices for implementing credit management strategies in small businesses include clearly documenting credit policies and procedures, communicating credit terms to customers, staying proactive in monitoring customer payments, and offering incentives for early payments. It’s also important to have a dedicated person or team responsible for managing and enforcing credit policies.

Q: How can small businesses deal with late payments and delinquent accounts?

A: Small businesses can deal with late payments and delinquent accounts by sending reminder notices, contacting customers directly to discuss outstanding balances, offering payment plans, and if necessary, seeking legal assistance or hiring a collections agency. It’s important to have a structured approach to managing late payments in order to minimize financial impact on the business.